Corequity provides independent, institutional equity valuation research. The results are used to screen for the best and worst values out of over 500 equities on a continuous basis. We have accumulated a proprietary database of historical monthly valuation data. For a brief background... http://corequity.blogspot.com/2013/05/some-background.html

Since inception in September 2004, the Undervalued Screens have outperformed the Overvalued by over 700 basis points per annum.

The last 12 months have been extraordinary in terms of performance. The Undervalued Screens have outperformed the Overvalued by close to 40%.

These tables show where the performance has come from in the two screens. The first shows the average percentage of Relative Strength (to the S&P 500) by Sector for the Undervalued. However, it is the second chart which shows each Sector of the Screen ranked by their total contribution to performance, i.e. the sum of the Relative Strength to the S&P 500. In this case the Industrials, Consumer Cyclicals and Technology are the top 3 Sectors

In the case of the Overvalued screens, the major contributors are Energy, Basic Materials and Industrials. An investment manager commented that the Energy Sectors poor performance was due to the weak prices but that doesn't take into account that the Energy equities were very overvalued given their normalized earnings.

Here is a look at the results for the May 31st screens in June.

January adds another 4 % to the spread between the Undervalued and Overvalued screens performance sine 6/30/16. This chart shows the relative performance to the average of our universe.

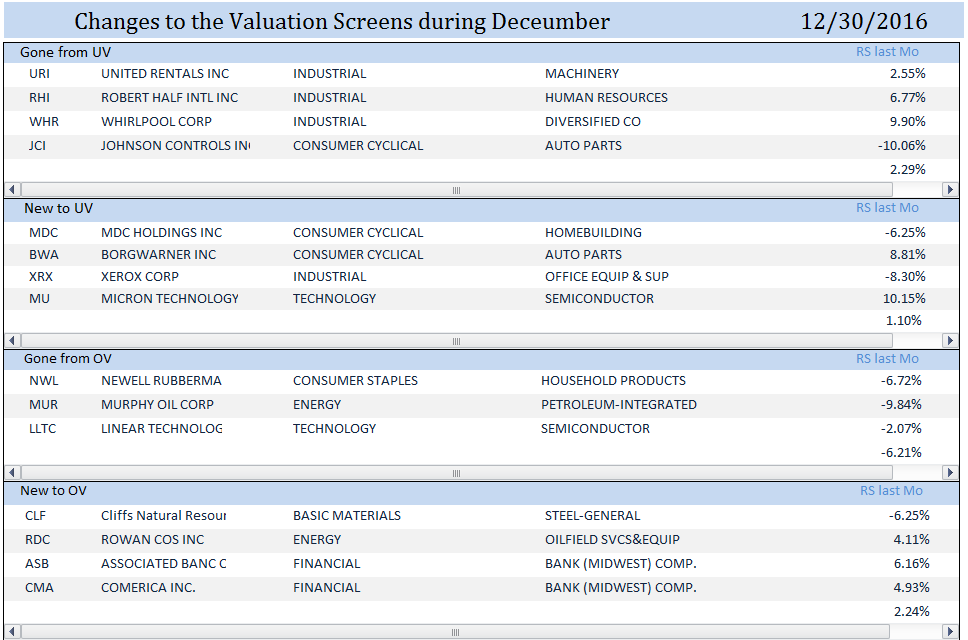

`

Here are summary tables showing which Sectors contributed to the superior performance of the Undervalued and the poor performance of the Overvalued.

The methodology is to add up the cumulative monthly Relative Strength[1] of the screened equities by company, industry and sector and rank the Sectors (in this case) by the total contribution to their performance over the period.

For more detail email corequity@gmail.com

(c) 2017 Robert L. Colby

[1] The percent change in price relative to the S&P 500

Conclusion: From the Shareholders perspective

most Stock Buybacks produce little benefit when compared to investing the same

funds in the company. They produce a onetime gain in Earnings per Share (usually

small) but contribute nothing to the growth of the Net Profit or Market

Capitalization. If a company is truly

unable to successfully invest the Buyback funds in its business, it would be

much better for the majority of shareholders to receive a Special Dividend.

For the

twelve months ending September 2016, total share buybacks were close to $600

billion for the S&P 500 companies. This

is an enormous amount of money being 66% of the earnings and only slightly less

than Fixed Capital Expenditures in the same period. The average buyback program resulted in a

“buyback yield” of just shy of 3%[1]. This resulted in a very modest annual decline

in the shares outstanding which led to an equally modest one time gain in

Earnings per Share for the Shareholders, i.e. the vast majority who did not sell

their shares.

Because

Buybacks and Dividend Yield are considered to be returns to the Shareholder

they tend to be lumped together in statements like the “Total Shareholder Yield

is currently close to 5% comprised of a 2% dividend yield and a 3% buyback

yield”.

This is very misleading. The source of funds for Buybacks are the

earnings and deprecation which should be first and foremost compared to what

they would have achieved if invested.

A 3% “Buyback

Yield” is greatly inferior to investing in the company’s business, acquisitions,

or a Special Dividend which would be shared by all Shareholders in hard dollars

as opposed the soft dollar benefit attributable to fewer shares.

Here is an

example of a typical S&P 500 equity. It has a market cap of $15 billion;

its shares are at 15x earnings and it buys back 3% of its outstanding shares. This is compared to a hypothetical but

typical Investment producing 3% in the 1st year, 8% in the 2nd

and 10% thereafter.

The share

purchase of 3% of the float produces a 3.5% pop in the EPS on day one. Annualized that is 3.5% in the first year, 1.7%

per annum in the second and so on. By

the second year, the Investment produces a higher return. By the 7th year, the Investment led to a Net Profit

of $985m which is almost double the first year’s investment while the Buyback

produced zero contribution to Net Profit.

Were the stock

price reduced by half and the Buyback amount kept the same you would get the

following result.

The original

gain in EPS is increased to 7% but it soon pales by comparison to the

Investment.

Using the

original price of $15 and twice the buyback funds ($1,000m), the result would

be the same as in Example 1 but the dollar gain in the Net Profit from Investing

would double as twice the funds were used.

These

hypothetical examples illustrate the mechanics of stock buybacks. Now let us look at two actual examples.

The first is Apple

as it is listed as the most aggressive in terms of dollar amount of funds spent

on buybacks in the last 12 months[2].

Despite Apple

having spent the over $30 billion, it confirms the disadvantages of Buybacks compared

to Investments. In this case we used the

average Return on Capital that they earned from 2009-15.

Now let us

look at one of the most aggressive buyback programs in terms of the percentage

of stock that was bought. Corning Inc. purchased

over 20% of their outstanding shares in the last 12 months[3]

which produces an initial gain of 27% in EPS on day one.

However, even

this aggressive program fails by comparison to the Investment after year three

even though their Return on Capital is only average.

One of the

reasons that investors are not more critical of stock buyback

programs may be because of by doing it year after year management creates the illusion that it is compounding. As shown here, the transactions are still a series of simple interest transactions.

The proof of

this is found in the Net Profit Test.

It answers the question:

What is the Required Rate of return on an

Investment of the funds, that would grow the Net Profit at the same rate that

the EPS grew due to fewer shares. Like

Apple, the answer is surprisingly low in most instances. We analyzed 30 Stocks

whose buyback programs resulted in a median decline of 25% of their outstanding

shares from 2008 to 2015. The median Required Return would have been only 4.9%.

The median

growth rate for their EPS was 7.7% pa while the Net Profit grew only at

2.4%. Instead, by investing at less than

5%, the Net Profit would have been 42% higher in the 7th year. Over

the seven years the cumulative gain in Net Profit would have been 1.8x the

original investment.

It doesn’t

make sense to put the growth of Earnings per Share ahead of the growth of Net

Profit and as a result, Market Capitalization.

The November 30th Undervalued stocks outperformed their counterparts by +3.3% to -1.5% for a spread of +4.8%.

It should be noted though that the Overvalued have over 50% of their representation in the Energy Sector which could lead to underperformance if, for example, energy stocks get a significant lift from positive ETF cash flows

There were huge gains and losses for those stocks entering or leaving the screens from October 31st to November 30th.

Those leaving the Undervalued averaged close to +14%. Those leaving the Overvalued were down 7%.

The 7 stocks entering the Overvalued screen increased an average of 29% in the month, an astonishingly high number. At the beginning of the month, they were fairly valued with an average of -1.8% and a range of -12 to +11%.

(c) 2016 Robert L. Colby

For the current Screens, contact robertlcolby@gmail.com

Our universe of stocks outperformed the S&P by 4.2% last month while the Undervalued Screen gained 6.5% relative. The Overvalued were equal to the universe' return of 4.2% mainly due to the superior performance of the Energy stocks which numbered 15 out of 26 in the screen.

The Overvalued ended the month on a strong note gaining 2.4% in the last week.

So far this month the Undervalued are ahead of the Overvalued by +6.5% to +1.8% relative to the S&P 500. However, the average of all stocks covered ouperformed the S&P by 4.5%. Compared to our universe, the Undervalued are +2.0% and the overvalued -2.7%.

This table shows the Sectors/Industries of strength and weakness for both.

The correlation

between a company’s percent change in outstanding shares from 2008-15 and

the rank of the CEO’s pay[1]

in 2015 was found to be -.18 in a sample of 100 S&P equities.

The reduction

in shares outstanding leads to an increase in Earnings per Share but not in Net

Profit. The correlation between the rank

in change in shares outstanding and the rank of EPS - Net Profit growth is .88.

The conclusion

therefore is that there is a tendency to pay CEO’s more for the illusion of

growth rather than growth itself.

An index for the monthly screens for value is created by linking the following months' average returns, excluding income. The Undervalued Screen index outperformed the S&P 500 by 395 basis points per annum while their counterparts, the Overvalued Screen index under-performed by the S&P by 158 basis points pa. The spread between them was 552 basis points

The index for our universe of stocks increase by an 193 basis points pa so the performance relative to that standard was +198 and -344% basis points respectively. The reason for the superior performance is most likely due to the unweighted universe vs the market weighted index.

10 Year Ranking among US Equity Funds*

To give an indication of how the returns on the Corequity Screens compared to managed accounts, we compared the 10 year returns to a universe of over 400 US equity funds as reported by the Globe & Mail for September 30th. The Undervalued's 10 year average was 8.51% vs 4.41% for the Overvalued. The Undervalued would have ranked in the 90th percentile (1st quartile) while the Overvalued would have been in the 24th or 4th quartile. Here the spread between them is 66 percentiles!

* Globe & Mail US equity funds with 10 year records.

A Simple Test to Dispel the Illusion Behind Stock Buybacks

Photo

A trader at the New York Stock Exchange in June. As shares have climbed, so have the prices companies pay to buy back their stock.CreditLucas Jackson/Reuters

Stock investors have had one sweet summer so far watching the markets edge higher. With the Standard & Poor’s 500-stock index at record highs and nearing 2,200, what’s not to like?

Here’s something. As shares climb, so too do the prices companies are paying to repurchase their stock. And the companies doing so are legion.

Through July of this year, United States corporations authorized $391 billion in repurchases, according to an analysis by Birinyi Associates. Although 29 percent below the dollar amount of such programs last year, that’s still a big number.

The buyback beat goes on even as complaints about these deals intensify. Some critics say that top managers who preside over big stock repurchases are failing at one of their most basic tasks: allocating capital so their businesses grow.

Even worse, buybacks can be a way for executives to make a company’s earnings per share look better because the purchases reduce the amount of stock it has outstanding. And when per-share earnings are a sizable component of executive pay, the motivation to do buybacks only increases.

Of course, companies that conduct major buybacks often contend that the purchases are an optimal use of corporate cash. But William Lazonick, professor of economics at the University of Massachusetts Lowell, and co-director of its Center for Industrial Competitiveness, disagrees.

“Executives who get into that mode of thinking no longer have the ability to even think about how to invest in their companies for the long term,” Mr. Lazonick said in an interview. “Companies that grow to be big and productive can be more productive, but they have to be reinvesting.”

Broadly speaking, those reinvestments appear to be in decline. Indeed, economists are concerned about the comparatively low levels of business investment since the economy emerged from the downturn more than seven years ago. This phenomenon may be attributable in part to the buyback binge.

One of the best arguments against stock repurchases is that they offer only a one-time gain while investing intelligently in a company’s operations can generate years of returns.

This is the view of Robert L. Colby, a retired investment professional and developer of Corequity, an equity valuation service used by institutional investors.

“The simplest way to evaluate a company’s asset allocation decisions over the years is to see whether its net profit growth is close to its earnings-per-share growth,” Mr. Colby said. “Unlike an investment in the business, share buybacks have no effect on net profit and there is no compounding in future years.”

Mr. Colby has developed an illuminating analysis that identifies a crucial difference between many truly successful companies and their underperforming counterparts. The exercise highlights the growth mirage that buybacks have on earnings-per-share measures. In addition, it shows that returns on investment need not be that large for a company to generate growth rates exceeding the evanescent earnings-per-share gains associated with buybacks.

In his test, Mr. Colby compared net profit growth and earnings-per-share gains at pairs of companies in the same industries from 2008 through 2015. In each case, he contrasted a company that bought back loads of shares during the period with another that did not.

One case study examined Cracker Barrel Old Country Store and Jack in the Box, two restaurant chains. Cracker Barrel bought back only $160 million worth of shares over the period while Jack in the Box repurchased $1.2 billion, reducing its share count by 37 percent.

Cracker Barrel passed the net profit test ably: Its growth in earnings per share over those years was 13.6 percent a year while its net income grew at a virtually identical 14 percent.

Jack in the Box made quite a contrast. Its annual earnings per share rose by 6 percent over the period, but its net profit declined by 0.5 percent a year.

To bring its net profit to the level of growth it showed in per-share earnings, Mr. Colby said, Jack in the Box would have had to generate after-tax returns of only 4.8 percent on the $1.2 billion it spent buying back shares. That doesn’t seem insurmountable.

Linda Wallace, a spokeswoman for Jack in the Box, said the company’s business model generated significant cash flow, “which our shareholders have told us they prefer to be returned to them in the form of share repurchases and dividends.”

She added that the average price the company paid to buy back its stock during the period was just under $37 a share, well below Friday’s closing price of $98.93.

Another notable buyback comparison was between Costco and Target, two large discount retailers. While Costco spent $2.7 billion to repurchase shares from 2008 through 2015, Target allocated $11.4 billion, reducing its share count by 20 percent.

Costco’s annual earnings-per-share gains of 9 percent during the period were almost identical to its 8.9 percent net profit growth.

Target’s numbers tell a different story. On the strength of its repurchases, Target’s earnings per share rose by 7.3 percent each year. Its annual net profit growth was just 4.3 percent, Mr. Colby found.

To close that gap, Mr. Colby calculated the after-tax investment returns Target would have had to generate on the $11.4 billion it spent on buybacks. The answer was a surprisingly nominal 5 percent.

Erin Conroy, a Target spokeswoman, said the company’s capital allocation priorities focus on “growing long-term shareholder value and supporting our enterprise strategy.” She cited Target’s practice of annual dividend increases and said that last year, the company added an infrastructure and investment committee to its board to provide more oversight of investments.

Testing for the buyback mirage is a worthwhile exercise for investors. That’s why it is the topic of a new program at the Shareholder Forum, which convenes independent workshops to provide information to help investors make sound decisions.

The net profit test, said Gary Lutin, a former investment banker who heads the forum, “cuts through to the essential logic of comparing a process that grows a bigger pie — reinvestment — to a process that divides a shrunken pie among fewer people: share buybacks.

“It’s pretty obvious,” he continued, “that even mediocre returns from reinvesting in the production of goods and services will beat what’s effectively a liquidation plan.”

Investors may be dazzled by the earnings-per-share gains that buybacks can achieve, but who really wants to own a company in the process of liquidating itself? Maybe it’s time to ask harder questions of corporate executives about why their companies aren’t deploying their precious resources more effectively elsewhere.

Altria Group (MO) spun off

Philp Morris (PM) in 2008 and the two have persued strikingly different asset

alllocation strategies since. PM has bought back 23% of their shares since 2008 while MO only bought back 5%.

As a result,

MO grew their EPS and Net Profit 61% and 52% respectively over the period. This contrasts to +33% and 0% for PM. Had PM invested the $28 billion that they used to buyback stock

at a 5.8% return, their 2015 Net Profit would have been $2.3 billion higher or

34% of what they achieved.

It should be noted that both

companies that both companies had a –ve correlation between the annual

percentage of the stock that they bought and the price they paid. This is the exception to the rule.

Note on Executive Compensation: PM’s average executive compensation over the last 5 years was 57% more than MO’s or $64.2 million vs$ 40.8[2].

Cigna vs Aetna

Cigna Corporation (CI) and Aetna (AET) also show a contrast in asset allocation. CI bought only 5% of their stock back whereas AET reduced their float by 23%. AET spent $10.3 billion vs $3.9 for CI. As a result, CI grew their Net Profit and EPS at nearly the same rate (+14.4% pa vs 13.3%). AET on the other hand grew their EPS at twice the rate of their Net Profit (10.1% pa vs 5.1%).

Due in part to the fact that AET was smart about timing

their buybacks, as shown by the negative correlation between the annual percentage

amount that they bought and the price,

the Required Rate to equalize the Net

Profit growth to their EPS is quite high at 9.1%.

Had they had achieved that, they would have earned $1 billion

more in 2015 than they did. If they had

earned only a 6% return, for example, the increase in Net Profit would have

been $624 million more or 23% above what they

achieved.

Note on Executive Compensation: AET paid their executives an average of $42.2

over the last five years, which was 17% more than the $36 million that CI

executives were paid.[4]

Costco vs Target

Costco (COST) spent $2.7 billion on stock buybacks from 2008-2015 but their shares outstanding increased by 1%. By contrast, Target (TGT) paid $11.4 billion to reduce their float by 20%. As a result, COST achieved almost identical growth in the EPS and Net Profit whereas TGT had a divergence of +7.3% vs +4.3% pa over the period.

Had TGT invested the $11.4 billion instead and earned a

return of 5.0%, they would have earned close to $700 million more in 2015, or

22% more than they did.

Note on executive compensation:

Can you guess which of these two companies paid their executives more?

Target paid their top executives 120% more than Costco did over

5 years! The average was $47 million

compared to $22 million. In 2015 alone

the comparison was $60 to $24 million![6]

Hypothesis: Executive compensation is positively correlated to the spread between the growth of Earnings per Share and the growth of Net Profit.

(c) 2016 Robert L. Colby

[1]

The required rate of return applied to the buyback funds to grow the Net Profit

at the same rate as the EPS.