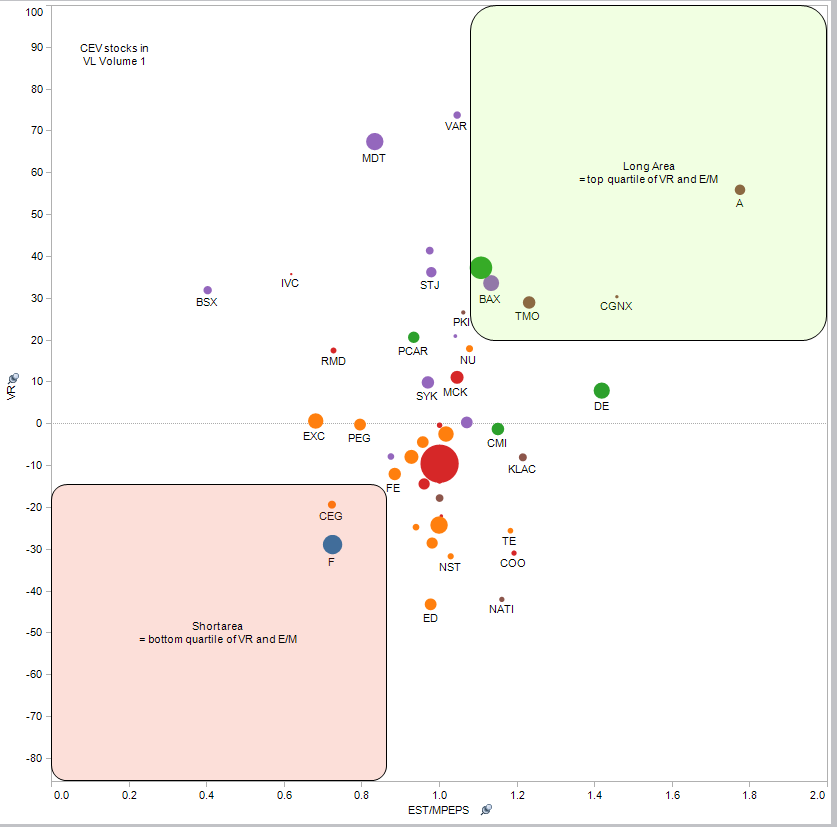

The Undervalued Screens outperformed the Overvalued by 9.2% per annum for the 7 years ending in September.*

Relative to our universe, the annualized returns were +3.2% pa vs -5.8% p.a. respectively. Relative to the S&P 500. the returns were +5.9% and -3.3% for the seven year period.

Performance data for other periods ending Sept 30th are show in the table below:

$100 invested in the both was would have been worth $150 and $79 respectively. Using only the top and bottom quartile for VR and E/M (4,4 vs 1,1) we get even larger returns and divergence. The values after seven years becomes $166 vs $68. The former screens would be closer to a portfolio returns while the latter are the buy & and sell or short lists.

* Returns are for the top bottom 2 quartiles for Valuation Return/Risk (VR) and the top and bottom quartile for E/M (the ratio of estimated earnings (EST) divided by normalized earnings (MPEPS)). Returns exclude income and are based on linked monthly average gains or losses.

Some background ...

In the late 1960s Robert co-founded Marcinvest Fund, a no load equity mutual fund in Canada. As manager, he developed a valuation methodology to ascertain whether street expectations were already discounted in the stock prices. In the early seventies Marcinvest was merged with Altimira Management and Robert continued as the sole equity manager.

In 1976, he moved to Boston to sell an institutional equity valuation service (under Colby Equity Valuations, Inc.). The valuation model was computerized in order to cover a large number of equities. Its primary goal is in identifying overvalued and undervalued equities.

The institutional clients who subscribed to the service included Allied Signal, Canadian Pacific, Canadian Broadcasting, General Electric, Ontario Hospital Association and Ontario Municipal Retirement System, Choate Hall & Stewart, Fidelity International, Fiduciary Trust Company, The First Church of Christ Scientist, Gardner & Preston Moss, Harvard Management Corporation, Jarislowsky Fraser, Massachusetts Financial Services, Thorne Ernst & Whinney, United Financial Management and Wellington Management. In addition, Robert was President of Manasset Corporation, a family office in Providence, RI. Mr. Colby’s equity valuation service was re-started over 7 years ago.

Robert Colby has had extensive corporate Board experience both as board member and officer of a number of for profit and non-profit organizations. A graduate of McGill University, he maintains residences in Dedham, Ma and Georgeville, Quebec.